The tax credits for research personnel are one of the most important tools for reducing the cost of R&D&I in companies. However, their practical application continues to raise questions: which profiles are eligible for the tax credit, what requirements must be met, and how to properly justify the activities in the event of an audit.

Beyond understanding what these Social Security tax credits for research staff entail, the truly critical issue is knowing how to apply them correctly.

In this guide, we walk you through the process step by step, taking a practical, business-oriented approach to identify the key requirements, common mistakes, and the necessary documentation to apply for the incentive successfully.

What are research staff bonuses?

Tax credits for research personnel allow companies toreduce Social Security contributions foremployees engaged in research, development, or technological innovation (R&D&I).

These are reductions in employers' Social Security contributions applicable toemployees engaged exclusively in R&D&I activities, and they are governed byRoyal Decree 475/2014.

They are part ofpublic policies aimed at promoting innovation andare designed to facilitate investment in technological talent.

Tax credits for research staff allow employers to reduce their contributions for general social security benefits and achieve savings ofup to 40%. This percentage can be increased to 50%in certain cases, such as for youngpeople under 30andfemaleresearchers, with anadditional 5%for each groupwhere applicable.

Current State of R&D Investment in Spain

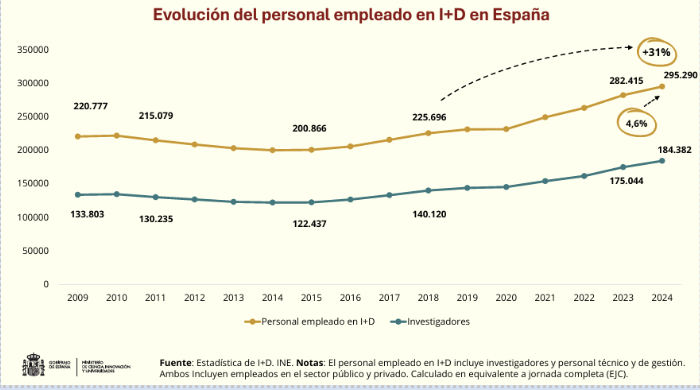

Spain ended 2024 with record-breaking figures for R&D investment, reaching a high of 23.931 billion euros, according to data from the Ministry of Science, Innovation, and Universities.

Growth is not limited to investment; the number of employees engaged in R&D activities increased by 4.6% compared to the previous year.

This reflects a steady trend that has been ongoing since 2018, with a cumulative increase of 31% in science and technology jobs.

This shows that companies are playing an increasingly important role in knowledge creation and in the country's competitiveness.

However, this momentum depends not only on corporate commitment, but also on making proper use of available incentives, especially those designed to reduce the cost of employing research staff.

In this context, Social Security rebates for research staff become a strategic tool.

Who is eligible to claim Social Security tax credits for research staff?

Companies that engage in R&D&I activities,regardless of their size or sector, andthat are headquartered in Spainare eligible for the tax credit, asit applies to employer contributions under the General Social Security System.

These organizations must meet certainlabor and technicalrequirementsrelated to the nature of their activities and the profile of their employees.

In this context, organizations such as the following are eligible for the incentive:

- Technology companies

- Startups focused on product development

- Organizations that drive internal innovation

It should be noted that when a company grants tax credits to10 or more researchers,the regulations require an additional step: obtaining aBinding Reasoned Report (IMV) from theMinistry of Science, Innovation, and Universities.

This report requires thatR&D&I projects have been previously certified by a certification body accredited by ENAC.

Once issued, the company has six months after the end of the fiscal year to submit it to Social Security.

Key point: It is not necessary to have a formal R&D&I department. What matters is that the activities areinnovative, systematic, and justifiable.

Requirements for applying for research staff bonuses

Before applying the research staff bonuses, it is essential to verify that the requirements set forth inRoyal Decree 475/2014 and Royal Decree-Law 1/2023 are met. These requirements are divided into hiring criteria and technical criteria:

Employment requirements:

For employment contractsentered into prior to September 1, 2023(Royal Decree 475/2014), the employee must:

- Have a permanent employment contract, an internship, or a fixed-term contract (with a minimum duration of 3 months).

- Belong to contribution groups 1, 2, 3, or 4 of the General Social Security System.

- Have a qualifying period of at least three consecutive months (for employees whose employment spans two fiscal years, the minimum is one month at the beginning or end of the fiscal year).

For new hireseffective September 1, 2023(Royal Decree-Law 1/2023), the requirements have been updated:

• The contract must be open-ended (the requirement to belong to contribution groups 1 through 4 is eliminated), with a maximum of three years of tax credits.

- Hiring researchers under the age of 30 results in an additional 5% tax credit

- Hiring female researchers carries an additional 5% bonus.

- Companies with 50 or more employees must have an Equality Plan in order to qualify for these additional percentages.

Technical requirements: the commitment of the research staff

The fundamental technical criterion, established inArticle 35 of Law 27/2014, is the employee’s engagement in activities classified as R&D&I.

Theallocation of resources toR&D&I activities must comply with the following parameters:

- At least 85%must be allocated to activities directly related to the implementation of R&D&I projects.

Up to 15%may be allocated to ancillary activities related to R&D&I that are not directly linked to a specific project. These include: technology watch, writing publications or doctoral theses, preparing patent applications, attending conferences, developing the company’s R&D&I plan, or, following the 2023 amendment, teaching.

Step-by-Step Guide to Applying Research Staff Bonuses

1. Identify eligible employees for the bonus

The first step is to determine which employees meet the hiring requirements (type of contract, contribution group, minimum duration) and the technical requirements (exclusive dedication to R&D&I).

Not all technical staff are eligible for the tax credit: there must be a direct and predominant link to research or technological innovation activities. The following must be analyzed:

- The actual duties of the position

- Participation in specific R&D&I projects

- The actual level of commitment.

2. Properly define R&D&I activities

It is essential to define which activities qualify as R&D or as Technological Innovation under Article 35 of Law 27/2014. R&D activities involve:

- Technical uncertainty

- The pursuit of new knowledge

- A systematic and structured approach organized as a project.

Technological innovation requires the development of technological advances in new products or processes, or substantial improvements to existing ones.

3. Verify the full-time employment requirement

One of the most stringent requirements is that staff must be effectively dedicated to R&D&I. Employees must not perform non-innovative operational tasks during the eligible period. There must be consistency between:

- His role in the company.

- Their participation in R&D&I projects.

- And the available activity logs.

4. Prepare the supporting documentation

The application for tax credits must be supported by solid technical and administrative documentation. The company must be able to demonstrate the following:

- The researcher's contractual relationship with the company during the eligible period.

- Identification and technical description of the R&D&I projects in which the research staff are involved.

- Roles and responsibilities of the research staff on each project.

- Evidence of the activities carried out

- Company organizational information.

Common mistakes when applying research staff bonuses

Despite its potential, many companies make mistakes that can result in refunds of contributions, penalties, and interest owed to Social Security.

Most common mistakes:

- Include staff who are not exclusively dedicated to R&D&I, or who combine production tasks with innovative activities without a clear distinction between the two.

- Failing to provide a technical justification for the activities carried out, or doing so in a general manner without linking them to specific projects.

- Confusing technological innovation with operational improvements or the company’s day-to-day activities.

- Lack of documentation linking the employee, their duties, and the R&D&I projects submitted.

- Automatic application of the discount without first verifying compliance with regulatory requirements.

- Include activities expressly excluded by the regulations, such as the implementation, production, corrective maintenance, or modification of existing software.

These errors are usually detected during review or inspection processes.

Eligibility for tax deductions and other R&D&I incentives

Bonuses for research staff may be combined with other incentives, such as:

- Tax deductions for R&D&I:provided for in Article 35 of Law 27/2014 on Corporate Income Tax. Specifically, companies that qualify as Innovative SMEs may combine both incentives for research staff who devote their entire workday exclusively to R&D activities within the company.

- Public grants: forexample, CDTI programs or other public funding programs, provided that the conditions of each call for proposals are met.

A combined approach to incentives allows companies to maximize the financial return on their R&D&I investments while simultaneously reducing labor costs and the tax burden associated with these activities.

How to Manage Research Staff Bonuses in a Technically Sound Manner

The proper application of bonuses for research staffrequires a technical, structured approach aligned with regulatory criteria.

For this reason, many companies choose to rely on specialized firms that enable them to:

- Verify that the activities qualify as R&D&I

- Ensure compliance with requirements

- Prepare comprehensive documentation

- Minimizing Risks During Inspections

In this context,ACERTAparticipatesin R&D&I projects by providing technical rigor, traceability, and security in the implementation of these types of incentives.

Frequently Asked Questions Frequently Asked Questions

- Up to 40% of the general contingency funds for research staff.

- It is not mandatory, but it is recommended to strengthen the technical justification.

- Yes, in many cases they are compatible.

- The company may be required to refund the discounts it has applied.

- Yes, provided they engage in genuine R&D&I activities and meet the requirements.