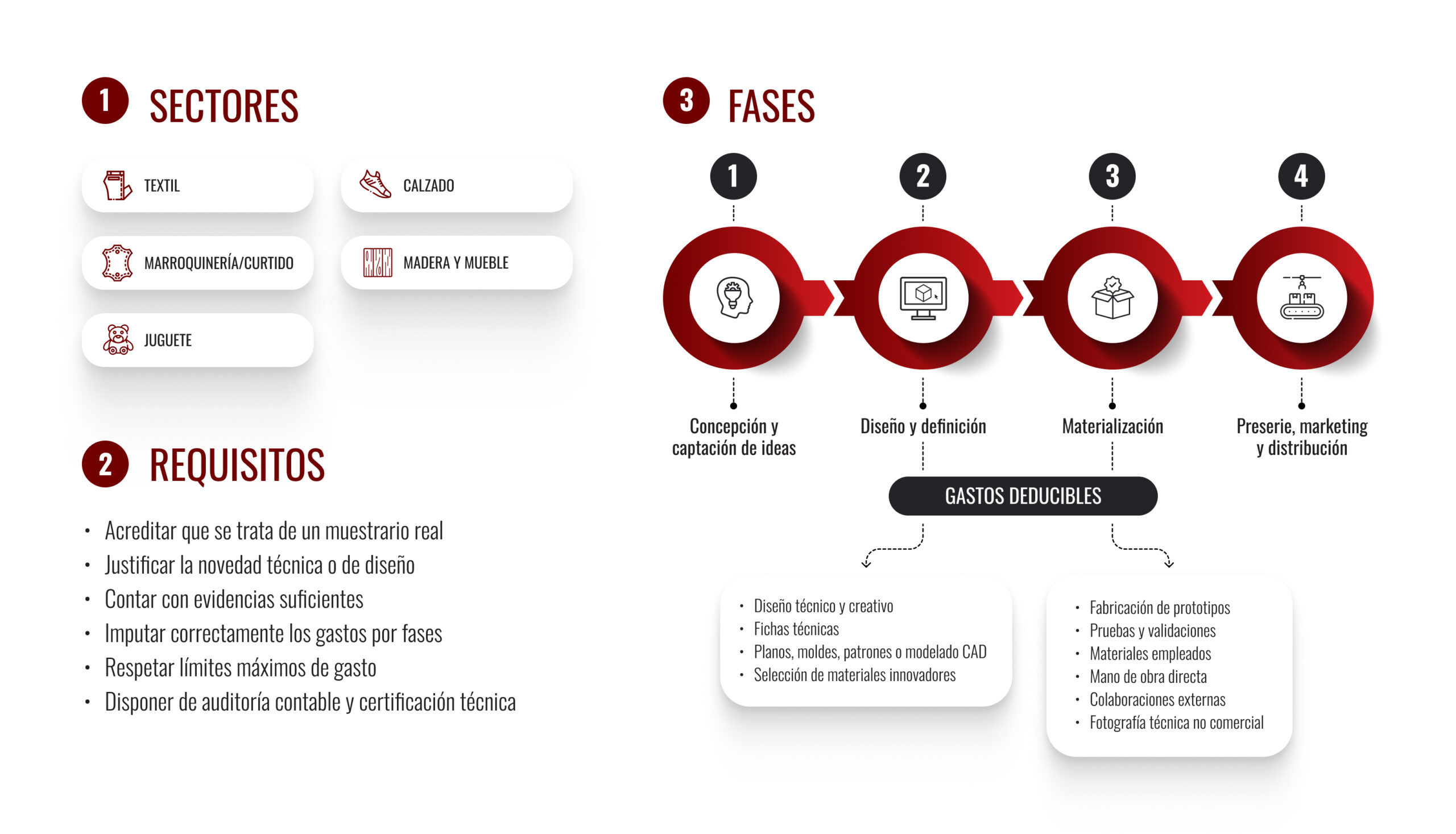

We certify the production of sample prototypes by companies in the textile, footwear, leather, leather goods, toy, furniture, and wood, to obtain a 12% tax deduction, provided that it is considered Technological Innovation, in accordance with Article 35 of Law 27/2014.

The development of product catalogs can generate direct and guaranteed tax savings for companies in the textile, footwear, leather, leather goods, toy, furniture, and wood sectors that create new product collections.

When the prototype meets the technical and documentation requirements set forth in the regulations, its development is considered a Technological Innovation (TI) activity, in accordance with Article 35 of Law 27/2014, they are allowed to apply a 12% tax deduction oncorporate income tax.

At ACERTA, we analyze, organize, and technically certify product samples so that companies can qualify for the Binding Reasoned Report (IMV) and and correctly apply tax deductions for catalogs with maximum legal certainty.

From a tax perspective, a sample falls under the Technological Innovation (TI) and is a set of prototypes developed to create, define, and validate new collections that have not yet been introduced to the market.

These are not commercial products intended for sale, but rather:

In this regard, tax deductions for the development of catalogs are based on the following legal framework:

The deductions for samples are particularly relevant in sectors with constantly updated product lines, such as textiles, footwear, leather goods and leather products, wood and furniture, or toys.

Its operation is simple, although each sector has specific technical criteria:

To claim the deduction, you must meet certain key requirements:

If your company launches new collections every year, you may be missing out on a significant tax incentive.

At ACERTA we assess the technical and tax feasibility of your product samples and guide you through the entire certification process and application of the deduction.

We perform a technical analysis and documentcomprehensive comprehensive to ensure that the sample book:

Do you want to have your sample books certified in order to claim a tax deduction?

Our approach combines technical rigor and proven experience with a proven track record.

Contact our technical team and find out how we can help you obtain your CAEs accurately, quickly, and with full assurance.

A prototype collection refers to the result of activities carried out to develop a set of prototypes that could potentially be turned into a new product.

12% of eligible expenses for technological innovation, in accordance with Article 35 of the Corporate Income Tax Act.

No. Only those related to Phase 2 (design and definition) and Phase 3 (prototype development).

It is not mandatory, but certification allows you to request a Binding Reasoned Report and provides greater legal certainty.

Yes. The deduction applies to the earlier design and prototyping phases (Phases 2 and 3), even if the collection has already been marketed.

Our team can analyze your case and guide you through the requirements, necessary documentation, and steps to begin the process with ACERTA. Contact us for a free consultation, and we'll respond within 24 hours.

If you have any questions, comments or suggestions, please do not hesitate to contact us.